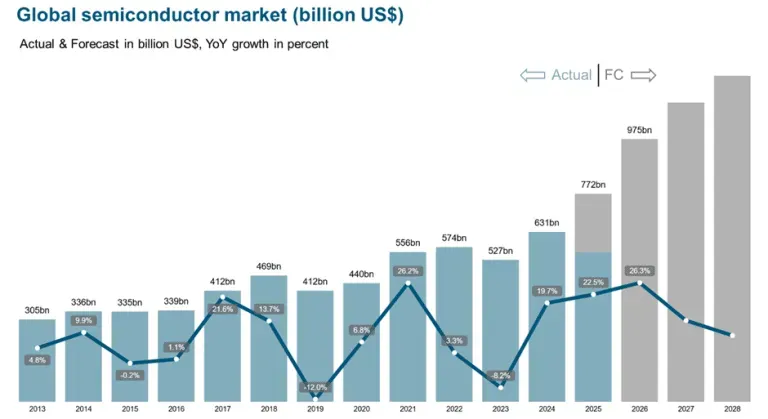

Semiconductor landscape in 2026 is shaping a world of accelerated compute, tighter supply chains, and policy-driven investments across major regions. For stakeholders tracking the semiconductor market 2026, demand is propelled by AI workloads, automotive electrification, and the rapid expansion of edge computing. The broader industry narrative highlights ongoing challenges in material provisioning, capital intensity, and the need for diversified sourcing. AI chips trends point toward specialized architectures, higher bandwidth memory, and energy-efficient accelerators that unlock new workloads. While the focus remains on performance, the sector’s next phase will depend on resilient ecosystems and smarter capacity planning.

Viewed through an LSI lens, the topic can be reframed as the evolution of silicon ecosystems, fabrication networks, and supply resilience rather than a single-node race. In practical terms, the narrative shifts toward regional manufacturing capabilities, vendor collaboration, and integrated packaging and testing that enable dependable silicon delivery. The emphasis moves to design toolchains, ecosystem health, and scalable capacity that supports AI, automotive, and industrial applications. The shift toward advanced nodes and fabs illustrates how capacity, yield, and cost management shape the industry’s longer-term trajectory. These relationships—policy, finance, talent pipelines, and cross-border cooperation—collectively define a robust, adaptable semiconductor landscape for the coming years.

1) Semiconductor landscape in 2026: drivers, demand, and digital transformation

The Semiconductor landscape in 2026 is being propelled by surging compute demand across AI, autonomous systems, and pervasive digitalization. AI workloads in data centers and at the edge push for higher performance, greater energy efficiency, and specialized architectures, which in turn informs the broader semiconductor market 2026. As chips become embedded in an expanding set of applications—from automotive electrification to smart devices—the demand mix continues to evolve, reinforcing the importance of a resilient chip supply chain 2026 and diversified sourcing.

Policy, geopolitics, and public-private investment add another layer of momentum. Governments worldwide chip in with incentives and programs that shape where, how, and with whom semiconductors are designed, manufactured, and deployed. This confluence of demand, policy, and investment highlights how the semiconductor market 2026 operates as a multi-faceted ecosystem where technology, economics, and national strategy intersect.

2) AI chips trends and architectures redefining compute in 2026

AI chips trends are redefining compute paradigms by prioritizing domain-specific accelerators, high-bandwidth memory, and efficient data movement. In 2026, specialized architectures and software ecosystems will influence how workloads are allocated between AI accelerators and general-purpose CPUs, driving improvements in energy per operation and throughput. This shift accelerates demand for advanced nodes and specialized packaging that can support high performance at scale.

The race for performance also spotlights design methodology and manufacturing efficiency. As AI workloads grow, design teams balance the lure of cutting-edge processes with cost, yield, and time-to-market realities. The resulting landscape reinforces the importance of EDA tooling, silicon-proven interoperability, and strategic partnerships across IP, design enablement, and manufacturing.

3) Chip supply chain 2026: resilience, diversification, and risk management

The chip supply chain 2026 remains characterized by fragility in critical segments, including material provisioning, wafer fabrication capacity, and equipment supply. To counter these bottlenecks, stakeholders are pursuing diversification—geographic scattering of production, multi-sourcing of critical materials, and greater inventory resilience. The semiconductor market 2026 consequently emphasizes supply chain visibility, risk assessment, and rapid response capabilities to maintain steady momentum.

Public policy and industry collaboration are essential to improving resilience. Government incentives, regional fab builds, and partnerships among foundries, IDMs, and gear suppliers are reshaping the ecosystem. Together, these efforts aim to reduce single-point vulnerabilities and create a more robust chip supply chain 2026 that can better withstand geopolitical disruptions and demand volatility.

4) Advanced nodes and fabs: optimizing performance, yield, and cost

The pursuit of smaller and more efficient nodes continues, with manufacturers racing toward true 3nm and 2nm processes where feasible. Yet the economics of lithography, mask costs, and thermal management push segments to optimized 7nm and 5nm platforms. The focus on advanced nodes and fabs remains central to the Semiconductor landscape in 2026, as plants expand capacity, upgrade toolsets, and pursue heterogenous integration to unlock higher performance at sensible power envelopes.

Packaging innovations and novel integration schemes also gain prominence. Silicon interposers, advanced cooling, and smarter packaging enable higher throughput without exploding die area or thermal load. The result is a more nuanced portfolio of solutions that blends process technology with system-level design to meet the ever-growing demands of AI, automotive, and edge computing.

5) Semiconductor manufacturing outlook 2026: capital expenditure and regional leadership

Capital expenditure in 2026 is fueling a multi-polar expansion of fabs and fabrication ecosystems. Regions pursuing supply diversification—particularly the United States, Europe, and select parts of Asia—are investing heavily in new crystalline growth facilities, lithography tooling, and cleanroom capacity. The semiconductor manufacturing outlook 2026 reflects a strategic recalibration toward regional leadership, balanced against global demand cycles and equipment availability.

Public-private partnerships and incentive programs accelerate facility builds, while equipment suppliers push for cost-effective, reliable solutions. This capex wave supports a broader goal: not only expanding capacity but also enabling more resilient, secure supply networks. The outcome is a rebalanced global landscape where geography, policy alignment, and supplier ecosystems determine who leads in advanced manufacturing and who continues to catch up.

6) Policy, geopolitics, and the semiconductor market 2026: funding, standards, and collaboration

Policy choices and geopolitics shape the semiconductor market 2026 in fundamental ways. Legislation such as the CHIPS and Science Act in the United States, EU programs, and national initiatives in Asia influence investment flows, workforce development, and which ecosystems are prioritized for critical technologies. Understanding the semiconductor market 2026 requires mapping these policy environments to supply chain dynamics and technology roadmaps.

Beyond funding, cross-border collaboration among foundries, fabless designers, equipment suppliers, and academic institutions remains essential. Shared standards, IP protection, and joint research programs help accelerate innovation while maintaining security and competition within a global ecosystem. The resulting dynamic explains why the chip supply chain 2026 embodies both resilience and fragility across different regions, depending on policy alignment and regional capabilities.

Frequently Asked Questions

What are the key drivers of the Semiconductor landscape in 2026, and how do AI chips trends influence demand?

Key drivers include surging compute demand from AI workloads, data centers, automotive electrification, and IoT adoption, complemented by policy incentives. AI chips trends—specialized architectures, high-bandwidth memory, and dedicated accelerators—expand the addressable market and intensify demand for energy-efficient, high-performance semiconductors, while ongoing supply constraints add a need for resilience.

In the Semiconductor landscape in 2026, how does the semiconductor market 2026 affect the chip supply chain 2026 and regional manufacturing strategies?

Broad demand across AI, automotive, and consumer electronics can strain materials, wafers, and equipment, keeping the chip supply chain 2026 fragile at key nodes. This drives regional manufacturing strategies toward fab expansion, diversification of suppliers, and public-private partnerships to improve resilience and ensure steady supply.

What role do advanced nodes and fabs play in the Semiconductor landscape in 2026, and what challenges remain?

Advanced nodes and fabs remain central to performance gains, with efforts focused on true 3nm and 2nm processes while balancing cost, lithography complexity, and thermal management. Global fabs are expanding capacity and adopting heterogenous integration, but packaging, cooling, and supply reliability continue to pose challenges.

What is the semiconductor manufacturing outlook 2026 for capex, fab expansions, and supply resilience?

The semiconductor manufacturing outlook 2026 signals higher capital expenditure as foundries and IDMs upgrade lithography, crystal growth, and cleanroom capacity. The emphasis is on regional diversification, resilient supply chains, and sustained partnerships to support long-term fab expansion and production stability.

How are policy decisions and geopolitics shaping the chip supply chain 2026 and ecosystem health within the Semiconductor landscape in 2026?

Policy actions like the CHIPS Act and EU programs influence investment flows, workforce development, and ecosystem prioritization, while geopolitics affect where capabilities are built. Collaboration among foundries, fabless companies, suppliers, and researchers remains essential to maintain momentum and ecosystem health.

What opportunities and risks do stakeholders face in the AI chips trends within the semiconductor market 2026?

Opportunities include faster AI deployment, energy-efficient accelerators, and new markets like automotive-grade chips. Risks involve supply chain disruptions, equipment shortages, and high capital costs. Successful players will pursue end-to-end solutions, diversified supplier networks, and strong ecosystem partnerships to balance risk and reward.

| Theme | Key Points | Implications |

|---|---|---|

| Global demand forces and application mix |

|

|

| Technology, nodes, and efficiency |

|

|

| Manufacturing capacity, capital expenditure, and supply resilience |

|

|

| Geopolitics, policy, and ecosystem health |

|

|

| Industry trends and strategic implications |

|

|

| Risks, opportunities, and stakeholder impact |

|

|

Summary

Semiconductor landscape in 2026 is shaping a complex, interdependent ecosystem driven by surging compute demand, persistent supply constraints, and policy-driven investments worldwide. The table above outlines the main themes—global demand and application mix, technology and efficiency, manufacturing capacity and resilience, geopolitics and policy, industry trends, and risks and opportunities—that together define how demand, technology, policy, and geopolitics intersect to create a dynamic, sometimes volatile market. The concluding outlook emphasizes continued diversification of nodes and supply, strengthened ecosystems, and strategic collaborations as the industry navigates an era of rapid change.